We remind you that the Director of Taxes had published on 15 September 2017 his circular L.G. - A n°63 concerning "Accounting obligations in tax matters". We have selected a few passages:

- "All transactions must be recorded promptly, accurately and completely and in date order, either in a single journal ledger or in a system of specialised journals,

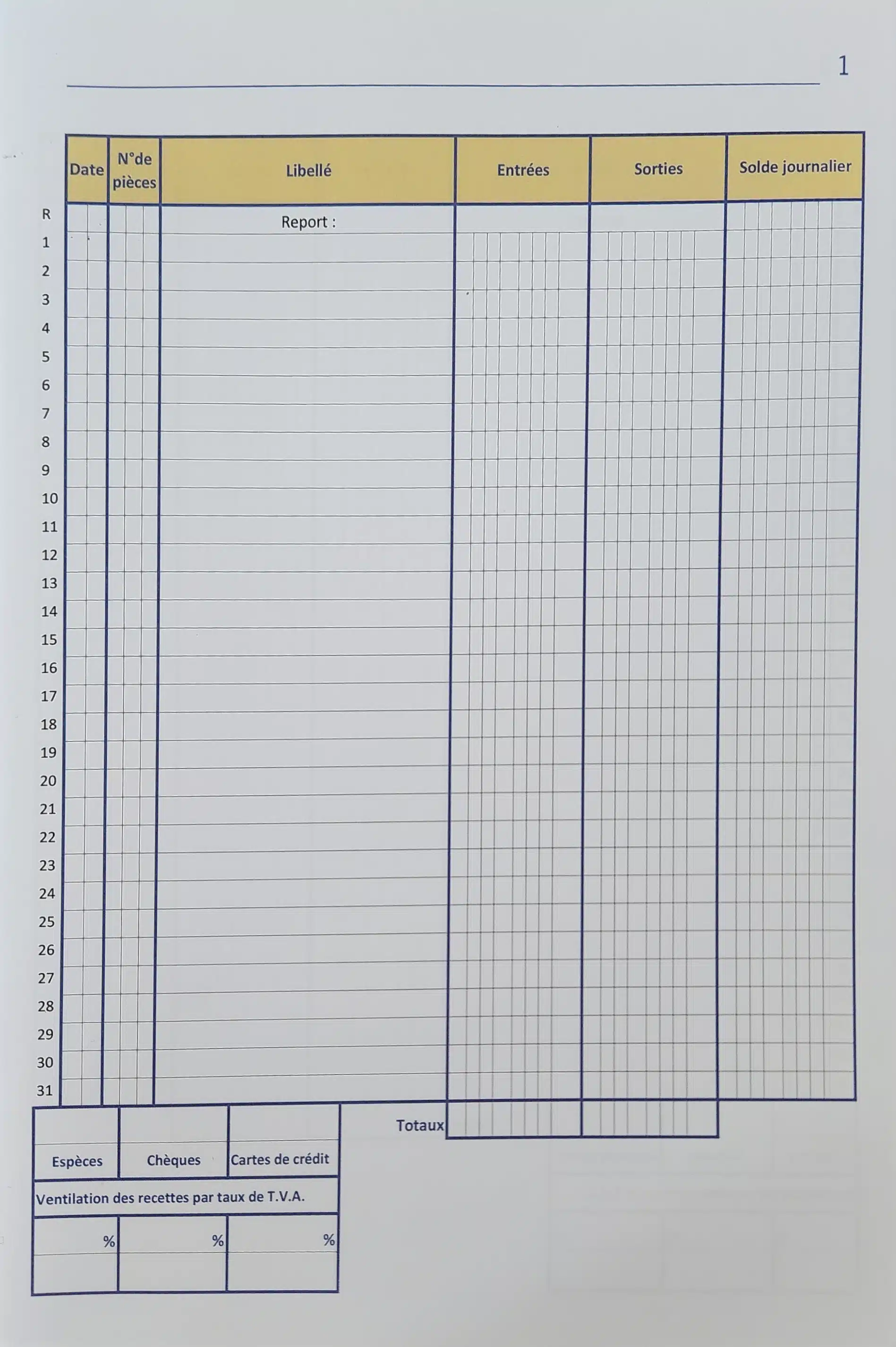

- "It should be noted that a cash book kept using a spreadsheet (e.g. Excel) is not authorised, as changes can be made at any time.

We would also remind you that the receipts in the cash book must correspond to the cash register statements, which you keep carefully with your accounting records.

In addition, we would like to inform you that if the tax authorities discover irregularities that result in tax reassessments, you run the risk of finding yourself in breach of Article 396 of the General Tax Law (Abgabenordung) as well as in breach of Article 506-1 of the Criminal Code.

Of course we remain at your disposal for any questions you may have and we are available to help you set up if you haven't already done so 😉

We have cash books for sale in 12 or 40 page versions, so please don't hesitate to ask.